by Brian Taylor, AuD, Editor-at-Large

Brian Taylor, AuD

As 2019 comes to a close and we inch closer to the FDA’s codification of over-the-counter (OTC) hearing aids, expected to occur in 2020, now is a good time for clinicians and business managers to create strategic plans that address some of the potential disruptions to the market.

Let’s start by taking a closer look at who might benefit from hearing devices sold directly to consumers. Although OTC hearing aids do not officially exist yet as a product category, there are plenty of ear-worn ampliers that can be purchased without seeing a licensed professional. These include hearing aids, PSAPs (this embedded link takes you to Oaktree’s useful PSAP database) and hybrid devices, sometimes known as hearables.

They might be labeled as PSAPs, but hybrid devices, which combine the features of consumer audio headphones with some of the essential features of traditional hearing aids, are different than many PSAPs that simply provide one function: basic amplification. Hybrid devices (hearables) typically have a core function and several secondary functions. The core function and the secondary functions vary with the person who is wearing the device and essentially turn any hearable, into a multi-tasking device.

For example, the core feature of a hybrid device could be listening to music from a favorite streaming service on your smartphone several hours per week (this might be the primary reason the consumer bought the device), however, a few times per week the hybrid device is used to talk on the phone, measure steps while exercising or amplify conversation in a crowded, noisy restaurant – all secondary functions.

Similar to high-end consumer audio headphones, these hybrid devices range in price from around $100 to over $500 dollars, much less expensive than traditional hearing aids. (As a sidenote, most modern hearing aids have direct streaming capability, which makes them hybrid as well, with the core function amplification and music streaming, etc secondary functions.)

Offering Hybrid Devices in the Audiology Clinic

The challenge for the business savvy audiologist is knowing if hybrid devices are worth offering to patients. The first step to better understanding if you want to provide these type of low margin devices in your clinic is to segment the market for hearing loss, a topic briefly mentioned in this informative 20Q. Here are some ideas on how you can segment consumers in your marketplace.

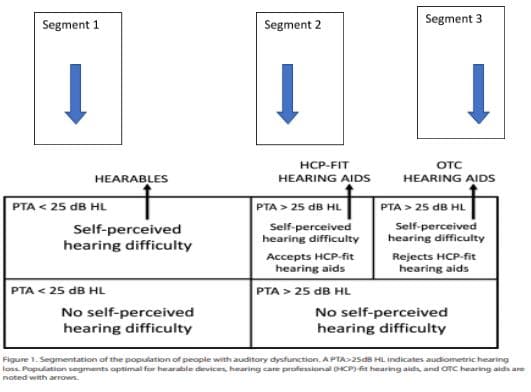

Figure 1 below, created by Dr. Brent Edwards of NAL, shows three different devices that correspond with three different potential segments of the market who might be considered candidates for each category of device. (Note in Figure 1 there are actually five segments of the market with the bottom two segments depicted in the figure perceiving no difficulty with their hearing and thus not yet in the market for purchasing any type of hearing device – even though use of a device is warranted.)

Segment 1 are individuals with pure tone averages better than 25 dB HL and self-perceived hearing difficulty. According to research, 25-plus million Americans fall into this segment: They have essentially normal audiograms but complain of an inability to hear, primarily in noisy places. Historically, because they have normal hearing thresholds on the audiogram, audiologists do not fit this group with hearing aids, but with the advent of hearables, this could be a market segment worth pursuing.

Segment 2 is comprised of individuals with worse than a 25 dB HL pure tone average and, as expected, a self-perceived hearing problem. These are the 10-12 million Americans hearing care specialists around the country are already serving quite well, according to the recently published Marketrak 10 report. Segment 3 are individuals with the same degree of hearing loss as those in Segment 2, but for some reason, reject the professional channel and the services provided by a licensed hearing care professional. Possibly, this is the segment of the population that gravitates toward (the yet to be codified) OTC hearing aids.

It is likely millions of Americans with hearing loss could fall into Segment 3 – it is commonplace in our industry to cite that just 20% of those with hearing loss wear hearing aids. Experienced clinicians know that a relatively large number of people within Segment 3 are likely to have complex communication difficulties and will eventually need counseling, as well as other types of professional services provided by audiologists and hearing aid dispensers. Perhaps many of the individuals in Segment 3 would prefer to dabble with amplification from the comforts of home and seek the services of an audiologist after experiencing some difficulties or questions with their OTC device.

Fig 1. Source: Edwards, B. Understanding new and emerging categories of hearing devices. ENT and Audiology News, Nov/Dec 2019.

The upshot of Dr. Edward’s segmentation chart above is there are three segments of the existing market for amplification devices, and hearing care professionals have built, until now, businesses that address just one of them (Segment 2).

For some practices, this may be enough to stay busy and generate a sustainable profit; for others their strategic plan needs to account for fresh marketing tactics that resonate with different groups of consumers with communication difficulties, the provision of hearables and unbundled professional services for those who first choose to purchase OTC, and then find they need customized service and support. More on this in Part 2.

Brian Taylor, AuD, is the director of scientific and product marketing for Sivantos. He is a veteran of the hearing industry with more than 25 years of experience, most recently at Fuel Medical Group where he served as Director of Clinical Audiology. An Audiologist since 1991, Brian received his Au.D. from Central Michigan University in 2006. During his career, Brian has been involved in many areas of the industry including clinical practice, practice and professional development, and training. Brian is a prolific and respected contributor to the industry with more than 25 publications and numerous speaking engagements both domestically and internationally. He has written and edited six textbooks, and most recently authored Essential Business Principles and Tactics for Clinical Managers: The First (or Next) 100 Days. Brian served as Editor-In-Chief at HHTM from 2018-2019 and currently serves as Editor-at-Large.